Quick Facts

- Commercial Approval: UnitedHealthcare currently leads the industry with a 52% approval rate for initial claims.

- Medicare Spending Cap: Starting in 2026, total annual out-of-pocket spending for Part D beneficiaries is capped at $2,100.

- Self-Pay Tier: For those without coverage, single-dose vials via LillyDirect now start at $299 per month.

- Employer Coverage: The share of employers with 5,000 or more workers covering GLP-1 medications for weight loss increased from 28% in 2024 to 43% in 2025.

- Legal Loophole: Utilizing an Obstructive Sleep Apnea diagnosis (ICD-10 G47.33) can often bypass specific obesity-only exclusions.

- Savings Window: The official manufacturer savings card remains valid for eligible patients through December 31, 2026.

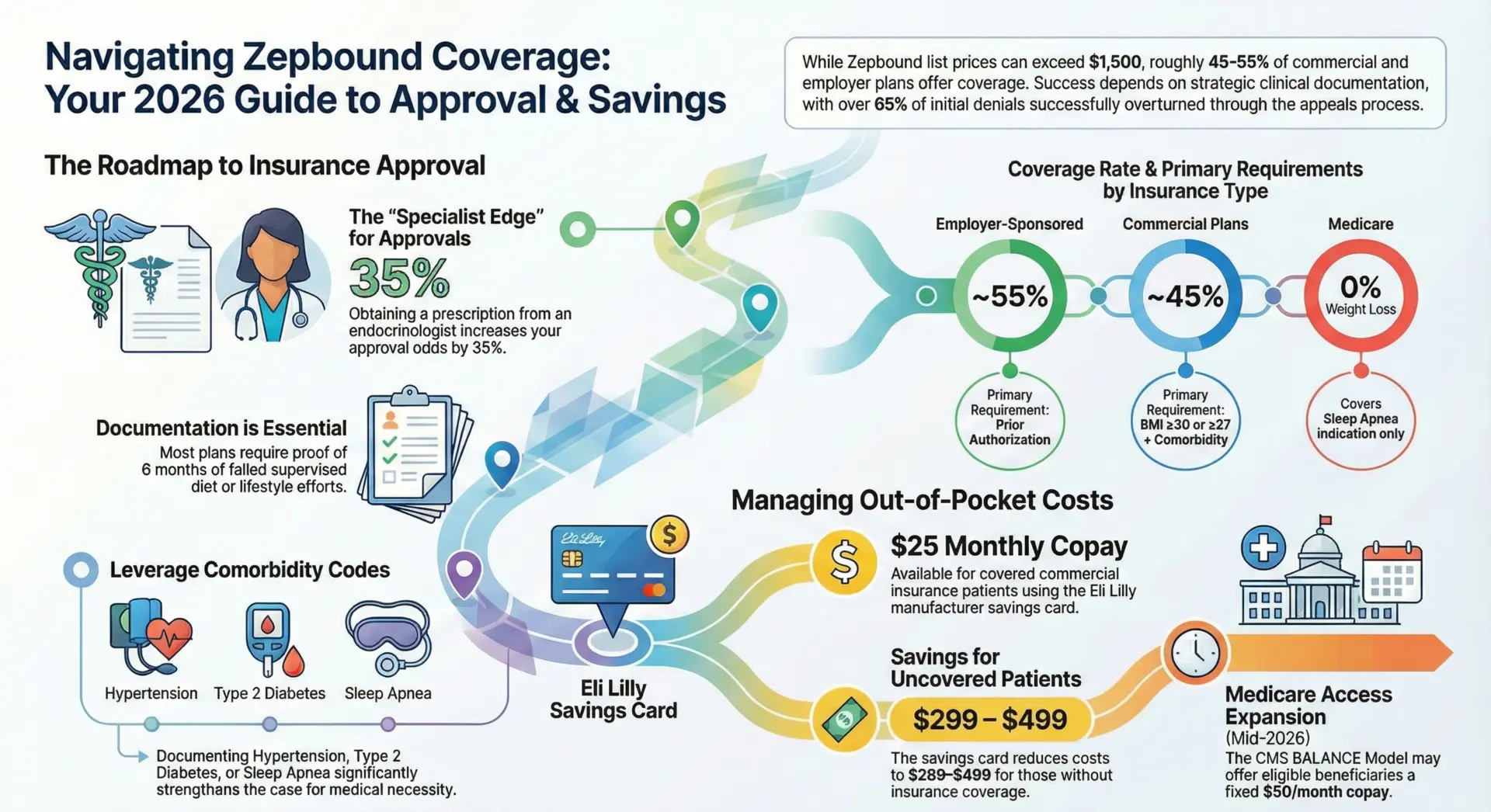

Zepbound insurance coverage in 2026 typically requires prior authorization and clinical documentation proving medical necessity, such as a BMI of 30 or higher, or 27 with weight-related comorbidities. By utilizing the Eli Lilly manufacturer savings card and navigating new federal programs like the CMS BALANCE model, patients can significantly reduce Zepbound out-of-pocket expenses to as little as $25 to $499 per month.

| Insurance Type | Expected Monthly Cost | Primary Hurdle | Coverage Probability |

|---|---|---|---|

| Commercial (Covered) | $25 - $150 | Prior Authorization (PA) | Moderate-High |

| Commercial (Not Covered) | $499 - $650 | Employer Exclusion | Low-Moderate |

| Medicare Part D | $50 (Fixed) or 25% Coinsurance | Statute Exclusions | Improving in 2026 |

| Self-Pay (LillyDirect) | $299 - $449 | Out-of-pocket expense | 100% (Cash only) |

Navigating Commercial Health Plans and Prior Authorization

If you are covered through an employer-sponsored plan, your journey to accessing Tirzepatide begins with the Pharmacy Benefit Manager. In 2026, the criteria for Zepbound insurance coverage have become more standardized yet more rigorous. Most major carriers like Aetna, Cigna, and UnitedHealthcare now mandate a comprehensive Zepbound prior authorization requirements and documentation guide that your physician must follow to the letter.

To maximize your chances of approval, data suggests that prescriptions originating from an endocrinologist or a certified obesity medicine specialist see a 35% boost in approval rates compared to general practitioners. This is largely because specialists are more adept at navigating step therapy protocols. These protocols often require you to try and fail on lower-cost alternatives, such as metformin or older weight-loss medications, before the insurer will greenlight a high-tier GLP-1.

You should also ensure your medical records include a documented history of participating in a supervised weight-loss program for at least six months. This serves as vital evidence for your clinical justification letter. It is worth noting that the landscape is constantly shifting; for instance, many patients faced hurdles after CVS Caremark’s 2025 decision to adjust its formulary placement for certain weight-loss drugs. Checking your plan’s 2026 formulary early is the best way to avoid surprises at the pharmacy counter.

When navigating employer-sponsored Zepbound coverage approval, remember that the plan design is ultimately chosen by your employer, not the insurance company. If your plan has a hard exclusion on weight-loss medications, no amount of medical necessity will force an approval. In these cases, your focus should shift toward the manufacturer's financial assistance programs.

The 2026 Zepbound Savings Card and Financial Assistance

For many, the manufacturer savings card is the only thing making this medication affordable. Eli Lilly has extended the Zepbound savings card eligibility for 2026 patients, providing a critical safety net for those with commercial health plans. If your insurance covers the drug, the card can reduce your monthly copay to as little as $25.

However, even if you are facing a denial, the program remains robust. For eligible patients with commercial insurance that does not cover Zepbound, the manufacturer's savings card can reduce the cost of a one-month supply of pens to as low as $499 through December 31, 2026. This is a significant relief, though it is subject to an $8,060 annual cap. If you hit this cap late in the year, your out-of-pocket costs may revert to the full retail price until the new year begins.

LillyDirect has also introduced a tiered pricing model for Zepbound vials, which are often cheaper than the auto-injector pens.

- 2.5 mg Zepbound vials: $299 per month

- 5 mg Zepbound vials: $449 per month

If you encounter a "denied" message at the pharmacy despite having the card, ask the pharmacist to use specific bypass codes (often referred to as Coordination of Benefits or COB fields). These codes tell the system to treat the savings card as a secondary payer. For those with very low income who lack any Zepbound insurance coverage, the LillyCares Patient Assistance Program (PAP) may provide the medication at no cost, though the eligibility requirements are strict regarding Federal Poverty Level thresholds. Utilizing your Health Savings Account (HSA) or Flexible Spending Account (FSA) is another smart way of reducing Zepbound out-of-pocket expenses, as these pre-tax dollars can be applied toward your annual deductible.

Medicare & Medicaid: The 2026 Regulatory Shift

Historically, Medicare beneficiaries were left out in the cold due to a decades-old statute prohibiting the coverage of weight-loss drugs. However, 2026 marks a turning point. The most significant change is the $2,100 out-of-pocket cap for Medicare Part D. Once you spend $2,100 on any covered medications, your plan must cover 100% of your remaining costs for the year.

Furthermore, the launch of the CMS BALANCE model in mid-2026 is designed to provide a bridge for access. This model allows participating plans to offer Medicare GLP-1 coverage under 2026 CMS BALANCE model guidelines, which can result in fixed $50 copays for eligible beneficiaries. This is a massive shift from the high coinsurance rates previously seen in the "donut hole" phase of Medicare coverage.

Another strategic avenue is the Sleep Apnea Loophole. Since Zepbound is now FDA-approved to treat moderate-to-severe Obstructive Sleep Apnea (OSA), Medicare plans are more likely to cover it when prescribed for this specific condition. If your physician uses ICD-10 code G47.33 and provides an Apnea-Hypopnea Index (AHI) score of 15 or higher, the medication is categorized as a treatment for a respiratory disorder rather than "weight loss," which bypasses the statutory exclusion.

Medicaid remains a patchwork of coverage. As of January 2026, only 13 state Medicaid programs in the United States provide explicit coverage for GLP-1 medications when prescribed for weight loss treatment. If you live in a state like California, which recently adjusted its GLP-1 policies, you must verify the latest preferred drug list (PDL) with your local administrator.

How to Appeal a Zepbound Insurance Denial

Receiving a denial letter is not the end of the road; it is often just the beginning of a negotiation. Statistics show that patients who appeal an initial rejection have a 65% success rate when they provide additional clinical documentation. The key is to speak the language of the insurance company.

Denial Decoder: The Appeal Toolkit

- Rejection Phrase: "Not medically necessary."

- Your Response: Provide lab results showing high A1C, hypertension, or high cholesterol. Use the term "metabolic health indicators."

- Rejection Phrase: "Plan exclusion for weight loss."

- Your Response: Shift the focus to a secondary diagnosis like Sleep Apnea (ICD-10 G47.33) or Cardiovascular Disease Risk.

- Rejection Phrase: "Failure to complete step therapy."

- Your Response: Document adverse reactions to previous medications (like GI upset from metformin) or provide proof that the alternative drug is contraindicated for your health history.

When you are documenting medical necessity for Zepbound insurance approval, your clinical justification letter should be specific. Instead of saying "the patient needs to lose weight," the letter should state, "The patient’s current BMI of 34, coupled with resistant hypertension, places them at a high risk for a major adverse cardiovascular event (MACE). Tirzepatide is required to mitigate this risk where previous interventions have failed."

A strategic approach to how to appeal a Zepbound insurance denial in 2026 involves persistence. Most insurance plans have three levels of appeal: internal review, a second internal review by a different medical director, and finally, an external independent review. Many approvals happen at the external review stage, where a third-party doctor evaluates the clinical evidence without the insurance company's financial bias.

FAQ

How much does Zepbound cost with insurance?

The cost varies based on your plan’s formulary and deductible status. If the drug is covered and you use the savings card, you could pay as little as $25 per month. If you have not met your deductible, you may pay the negotiated rate (often $500–$900) until the deductible is satisfied, after which your standard copay applies.

Does insurance cover Zepbound for weight loss?

Coverage depends entirely on your specific employer-sponsored plan or state Medicaid policy. While more employers are adding coverage—up to 43% for large firms—many still exclude weight-loss medications. If your plan covers anti-obesity medications, you will still likely need to meet BMI and comorbidity requirements for approval.

Is Zepbound covered by Medicare?

Medicare generally does not cover Zepbound when prescribed solely for weight loss. However, it may be covered under Part D if prescribed for a related condition that Medicare does recognize, such as Obstructive Sleep Apnea. Additionally, the 2026 CMS BALANCE model is introducing new pathways for fixed-cost access for certain beneficiaries.

What is the Zepbound savings card program?

This is a manufacturer-sponsored program by Eli Lilly that reduces out-of-pocket costs for patients with commercial insurance. It can lower the price to $25 for those with coverage or to $499 for those whose insurance excludes the drug. It is not available to those on government-funded plans like Medicare or Medicaid.

Why did my insurance deny coverage for Zepbound?

Common reasons for denial include plan-wide exclusions for weight-loss drugs, failure to meet BMI criteria, or not completing "step therapy" with cheaper medications first. Denials can also occur due to simple clerical errors or missing documentation in the initial prior authorization request.

What are the requirements for Zepbound insurance approval?

Standard Zepbound prior authorization requirements usually include a BMI of 30+ or a BMI of 27+ with a comorbidity like type 2 diabetes or hypertension. You must also show proof of failure in a supervised lifestyle modification program and have your doctor submit a formal request highlighting your medical necessity.